A Simple, Number-Driven Guide Using Real Equity Examples

Introduction: Why Valuation Matters (But Should Come Last)

Many investors start with valuation. This is a mistake.

Valuation only makes sense after you understand the business, its financial strength, and its risks. Valuation does not tell you what to buy — it tells you whether you are paying a reasonable price.

Think of valuation as:

A price check, not a quality check.

This article explains valuation simply, using two core tools:

- P/E (Price-to-Earnings)

- DCF (Discounted Cash Flow)

What Valuation Is (In One Line)

Valuation is the process of estimating what a business is worth today, based on the cash it can generate in the future.

It is not prediction — it is expectation management.

Two Valuation Tools You Actually Need

Ignore dozens of ratios. Start with just these two:

- P/E Ratio → Fast, comparative, imperfect

- DCF Model → Logical, assumption-driven, powerful

Part 1: P/E Ratio (The Simplest Valuation Tool)

What Is P/E?

P/E = Price per Share ÷ Earnings per Share

It tells you:

How much investors are willing to pay for ₹1 or $1 of earnings.

Question: What does a high or low P/E really mean?

What to look for:

Check whether the company has high growth, high stability, or high risk. P/E alone means nothing without context.

Example 1: NVIDIA (High Growth Case)

Let’s use simplified, rounded numbers.

- Share Price: $900

- Earnings Per Share (EPS): $30

P/E = 900 ÷ 30 = 30x

How to Interpret This

A P/E of 30 means:

- Investors are paying $30 for every $1 NVIDIA earns today

- Market expects very high future growth

Question: Is a P/E of 30 expensive?

What to look for:

Compare P/E with future earnings growth, not past earnings.

If NVIDIA’s earnings grow at 25–30% annually, a P/E of 30 may be justified.

If growth slows to 10%, the same P/E becomes risky.

Example 2: Alphabet (Mature Quality Case)

Simplified numbers:

- Share Price: $150

- EPS: $7.50

P/E = 150 ÷ 7.5 = 20x

How to Interpret This

A P/E of 20 suggests:

- Moderate growth expectations

- High business stability

- Strong cash generation

Question: Why does Alphabet trade at a lower P/E than NVIDIA?

What to look for:

Growth speed and business maturity.

Alphabet is massive and stable, but not growing as explosively as NVIDIA. Lower growth → lower P/E.

When P/E Works Best

P/E works well for:

- Profitable companies

- Stable earnings

- Industry comparisons

It works poorly for:

- Loss-making companies

- Cyclical businesses at peak earnings

- Early-stage growth firms

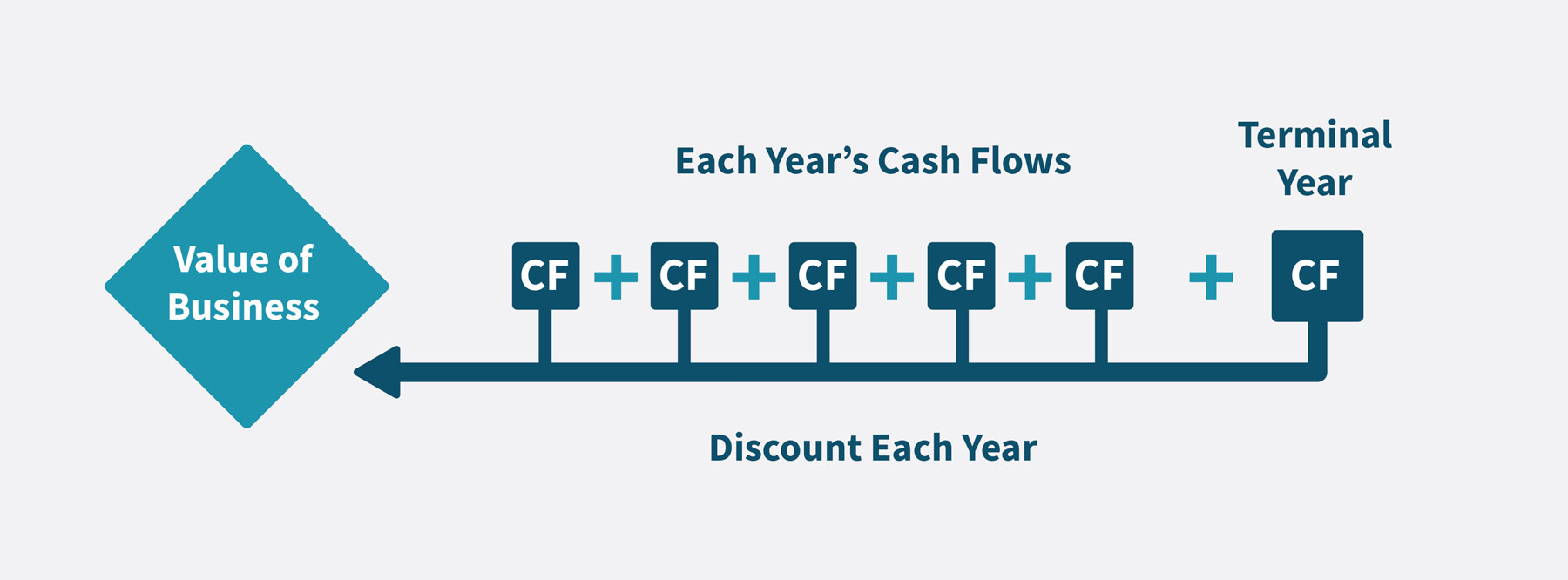

Part 2: DCF (Discounted Cash Flow) — The Logical Method

What Is DCF (In Simple Words)

DCF estimates what a company is worth by:

- Estimating future cash flows

- Discounting them back to today’s value

It answers:

“If this business generates cash in the future, what is that worth today?”

Question: Why discount future cash?

What to look for:

Money today is worth more than money tomorrow due to risk, inflation, and opportunity cost.

A Simple DCF (Without Math Overload)

Let’s do a very simplified DCF-style thinking.

Example: Alphabet (DCF-Style Thinking)

Assumptions (simplified):

- Current Free Cash Flow: $70 billion

- Expected growth: 8% per year for 10 years

- Discount rate: 10%

Step 1: Estimate Future Cash

If Alphabet grows cash flow at ~8%:

- Year 1: $75.6B

- Year 5: ~$103B

- Year 10: ~$151B

Step 2: Discount to Today

Future cash is discounted because:

- Growth may not happen

- Competition exists

- Regulations can change

After discounting, assume present value ≈ $1.4 trillion (illustrative).

Step 3: Compare with Market Value

If Alphabet’s market cap:

- Is below $1.4T → potentially undervalued

- Is far above $1.4T → optimistic assumptions already priced in

Question: What makes DCF dangerous?

What to look for:

Small changes in growth or discount rate create huge valuation changes.

DCF is powerful — but very assumption-sensitive.

Example: Why DCF Is Tricky for NVIDIA

NVIDIA:

- Has explosive recent growth

- Faces cyclical demand risk

- Depends on AI spending cycles

Question: Why is DCF risky for NVIDIA?

What to look for:

When growth is uncertain or extreme, DCF outputs can be misleading.

For such companies:

- Use ranges, not single values

- Combine DCF with P/E and growth reality

Practical Valuation Rules (EquiDeck Standards)

Rule 1: Valuation Comes After Business Understanding

Never value a company you don’t understand.

Rule 2: Use P/E for Sanity Checks

P/E helps answer:

“Am I paying too much compared to history or peers?”

Rule 3: Use DCF for Direction, Not Precision

DCF tells you:

- Cheap vs expensive

- Margin of safety

- Sensitivity to assumptions

It does not give exact prices.

Common Valuation Mistakes

❌ Mistake: Low P/E = Cheap

What to look for instead:

Check if earnings are temporary or declining.

❌ Mistake: DCF Shows Upside = Buy

What to look for instead:

Check if assumptions are realistic and conservative.

❌ Mistake: Ignore Growth Quality

What to look for instead:

Sustainable growth beats fast but fragile growth.

A Simple Valuation Mental Model

A great company can be a bad investment at the wrong price.

An average company can be a good investment at the right price.

Valuation bridges this gap.

Final Thoughts: Valuation Is a Tool, Not a Verdict

Valuation does not tell you what will happen.

It tells you what is already expected.

When expectations are too high, risk increases.

When expectations are reasonable, opportunity appears.

At EquiDeck, valuation will always be:

- Conservative

- Assumption-aware

- Used alongside business quality

0 Comments